Budgeting

Budget Like You Mean It

How to Make a Budget: Your Step-by-Step Guide

Learning how to budget might seem overwhelming, but hear this: You can do it. Here's how to make a budget in just five steps.

Read ArticleTrending Budgeting Articles

What Is a Budget?

5 Proven Ways To Achieve Financial Security

Why Are Food Prices Going Up?

The Cheapest Grocery Stores in America 2024

21 Housewarming Gifts They’ll Love for Under $25

Budgeting Apps Comparison 2024

6 Best Money Hacks of 2024

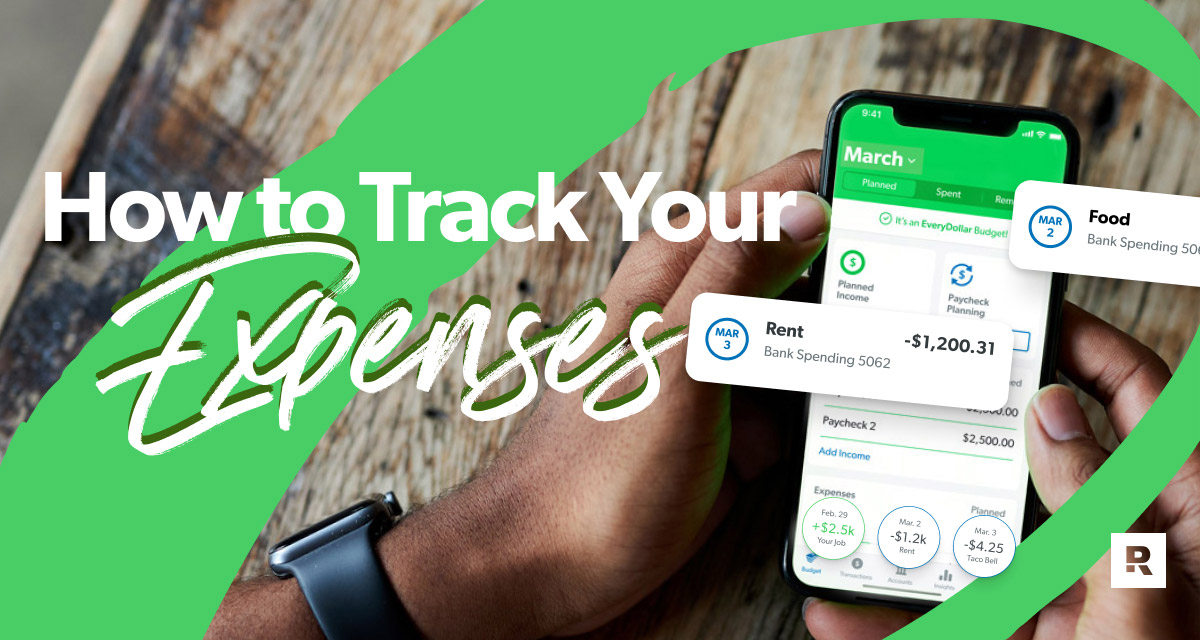

How to Track Expenses in Four Simple Steps

More Budgeting Resources

Downloadable Budgeting Forms

If you like spreadsheets, these helpful budgeting forms are for you!

Free Easy-to-Use Budgeting Tool

Take control of your money by planning where it should go every month.

Make Budgeting Easy

Check out the Complete Guide to Budgeting, and take the stress out of it.